Turning Clouds into Banks

The fintech moment for cloud computing

TL;DR

The cloud is ripe for disruption in its second act. PaaS companies are poised to do to AWS what Stripe did to banking – simplify, innovate, and explode. Welcome to cloud computing's fintech moment.

The Evolution of Banks and Fintech

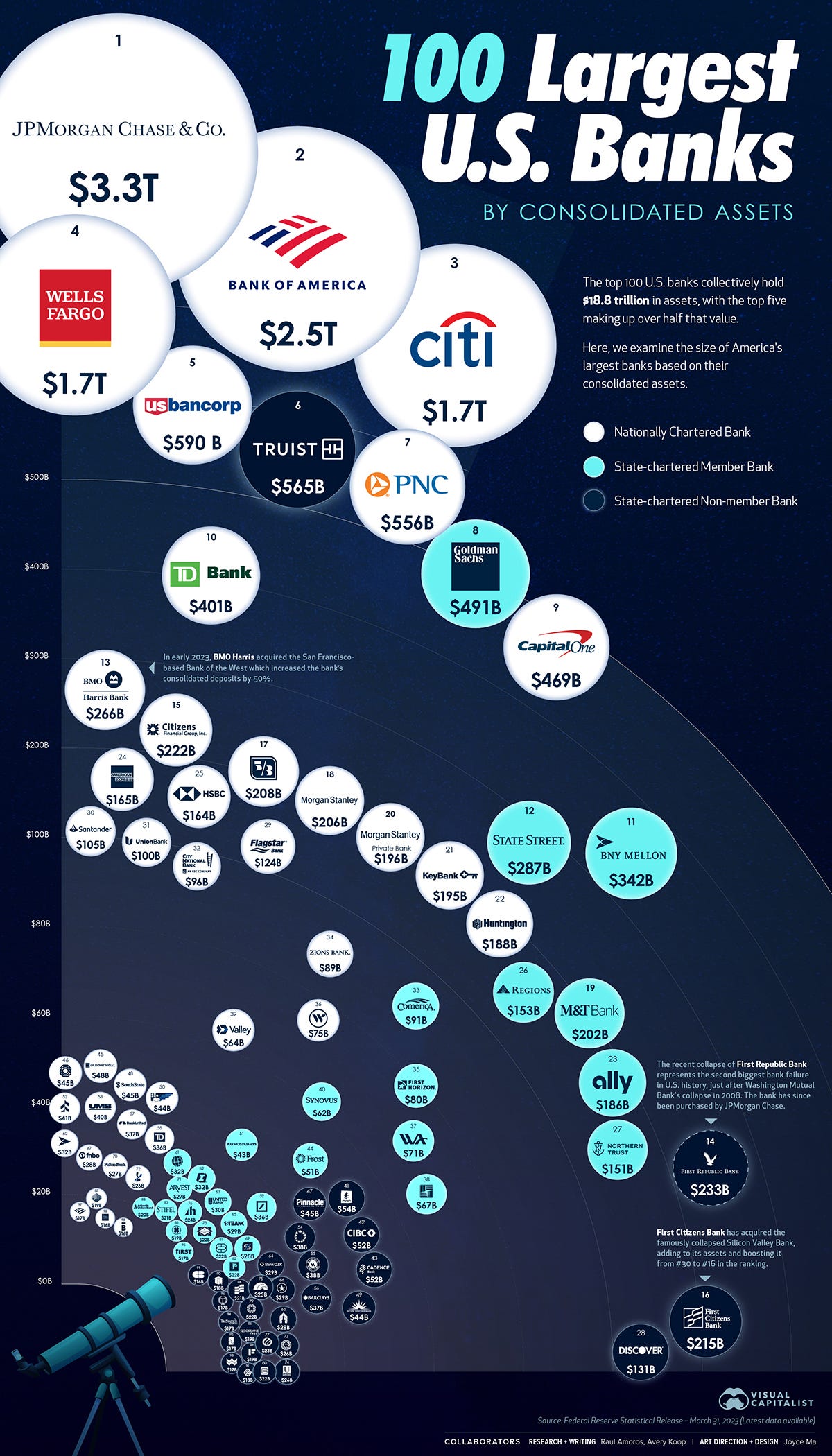

Historical Context of Banking

Banks have indeed existed for millennia, with early forms of banking traced back to ancient civilizations. The first known bank-like institution dates back to 2000 BC in Assyria and Babylonia. Throughout history, banks have served essential functions in society:

Facilitating payments

Providing investment opportunities

Offering loans

Providing insurance services

The Smartphone Revolution and Financial Access

The advent of smartphones in the 21st century dramatically changed the landscape of financial services:

By 2021, there were 6.378 billion smartphone users worldwide, accounting for 80.63% of the global population.

Mobile payment transaction value is expected to grow from $1.97 trillion in 2021 to $11.83 trillion in 2028.

Friction in Traditional Banking

Despite their long history, traditional banks have faced challenges in adapting to the digital age:

In 2019, 25% of U.S. households were unbanked or underbanked.

66% of millennials consider their conventional bank's digital offering to be average or below average.

The Rise of Fintech

This gap in service created opportunities for fintech companies to disrupt various banking niches while using banks as their platform:

Point of Sale (POS) Devices:

Square, founded in 2009, reached a market cap of $97.92 billion by 2021[6].

Peer-to-Peer Payments:

Venmo, acquired by PayPal in 2013, processed $230 billion in total payment volume in 2021[7].

Buy Now, Pay Later (BNPL):

The BNPL market is expected to grow from $141.8 billion in 2021 to $995.1 billion by 2026[8].

Fintech Giants and Their Impact

Several fintech companies have become major players in the financial services industry:

PayPal: Founded in 1998, had 426 million active accounts by Q4 2021.

Stripe: Valued at $95 billion in 2021, making it the most valuable private fintech company in the U.S.

Chime: Reached 12 million users by 2021, becoming the largest neo-bank in the U.S.

And there are many more here disrupting different niches

Changing Financial Landscape for Younger Generations

The fintech revolution has particularly impacted younger generations, since GenZ phones are more accessible than banks:

88% of GenZ use mobile banking apps, with 75% of them using digital banking as their primary banking channel.

Cash App, developed by Square, had over 70 million annual transacting active customers in 2021.

Case Study: Peer-to-Peer Payments

Let’s take a look at the P2P payments example:

The Old Way: Banks and Traditional Methods

Before the fintech revolution, transferring money between individuals was a cumbersome process:

1. Cash: Required physical presence, risky for large amounts.

2. Checks: Slow to clear, could bounce, needed physical delivery.

3. Bank wires: Expensive, required a trip to the bank, complex for international transfers.

4. Money orders: Fees for purchase, limited availability.

These methods were particularly problematic for:

People without easy access to bank branches

Those needing to send money quickly

Individuals making frequent, small transfers

Anyone trying to send money internationally

The system was slow, expensive, and often excluded those without traditional bank accounts.

The PayPal Disruption

PayPal, founded in the late '90s, was one of the first to challenge this status quo:

Introduced email-based money transfers

Created a digital wallet concept

Integrated with e-commerce platforms

Offered lower fees than traditional methods

PayPal made it possible to send money instantly, without the need for a bank account. This was a game-changer for many, especially in the burgeoning world of online commerce.

The Modern P2P Ecosystem

Following PayPal's lead, a wave of fintech companies further revolutionized P2P payments:

1. Venmo: Made splitting bills and sharing expenses social and fun.

2. Cash App: Expanded beyond payments to include investments and cryptocurrency.

3. Zelle: Brought rapid, fee-free transfers directly to bank accounts.

These platforms addressed key pain points:

Speed: Transfers often completed in minutes, not days.

Accessibility: Available to anyone with a smartphone, often without needing a bank account.

Cost: Many transfers became free or very low cost.

Convenience: No need to visit a bank or even know someone's bank details.

The Impact

This fintech disruption in P2P payments had far-reaching effects:

1. Financial Inclusion: Provided banking-like services to the underbanked.

2. E-commerce Growth: Enabled easy payments for small businesses and individuals online.

3. Gig Economy: Facilitated quick payments for freelancers and gig workers.

4. International Remittances: Made cross-border transfers faster and cheaper.

5. Reduced Cash Usage: Accelerated the shift towards a cashless society.

By addressing the shortcomings of the traditional banking system, fintech companies transformed P2P payments from a slow, expensive process into a quick, easy, and often free service accessible to almost anyone with a smartphone. This democratization of financial services exemplifies how fintech has disrupted and improved upon the traditional banking model.

Now that we have established this lets take a look at where the public cloud services are today.

The Disruption of Traditional Cloud Services

The Current State of Public Cloud Services

Just as traditional banks dominated the financial landscape, companies like Amazon Web Services (AWS), Google Cloud Platform (GCP) and others have become the giants of cloud computing. While they offer powerful and scalable solutions, they also present challenges:

1. Complexity:

Vast array of services and options

Steep learning curve for configuration and management

Requires specialized knowledge and certifications

Hard to operate securely

2. Cost:

Complex pricing models

Easy to incur unexpected costs

Often requires dedicated teams for cost management

Often you end up paying for something you don’t need

3. Inequity:

Favors large enterprises with resources to manage complexity

Challenging for small startups and individual developers

High upfront knowledge investment required

The Rise of PaaS and Simplified Cloud Services

Similar to how fintech companies disrupted traditional banking, a new wave of Platform as a Service (PaaS) and simplified cloud services providers are challenging the status quo:

1. Replit:

Offers a browser-based coding environment

Simplifies deployment and hosting

Makes collaboration easier, especially for beginners

2. Vercel:

Specializes in frontend deployment and hosting

Streamlines the process of deploying web applications

Offers easy integration with popular frameworks

Simplifies serverless application development

Provides a unified experience for building full-stack applications

Reduces the complexity of working with AWS services

4. Heroku:

Pioneered easy application deployment

Abstracts away much of the infrastructure management

Offers a straightforward pricing model

Provides a simpler, more user-friendly interface

Offers predictable pricing

Caters to developers and small to medium-sized businesses

And so many more providing vertical focus (neon, val.town, supabase etc.) or horizontal abstractions (Civo, Scaleway, Linode etc.)

How These Companies Are Disrupting Cloud Services

These new players are transforming cloud computing in several ways:

1. Simplification:

Abstract away complex infrastructure details

Provide intuitive interfaces and workflows

Reduce the learning curve for cloud deployment

2. Cost Transparency:

Offer clearer, more predictable pricing models

Provide free tiers for small projects and learning

Reduce the need for dedicated cloud management teams

3. Democratization:

Make cloud services accessible to individual developers and small teams

Enable rapid prototyping and deployment

Lower the barrier to entry for cloud computing

4. Focus on Developer Experience:

Streamline the development-to-deployment pipeline

Offer integrated development environments

Provide better tools for collaboration and version control

5. Specialization:

Cater to specific use cases (e.g., frontend deployment, serverless applications)

Optimize for particular development workflows or frameworks

This is very similar to newer fintechs going VERP

Case Study: Building and Deploying a Web App on GCP vs Replit

Scenario

Let's consider a scenario where a developer wants to build and deploy a simple web application. The app is a basic todo list application built with Node.js, using Postgres for data storage.

The Old Way: Google Cloud Platform (GCP)

Step 1: Setting Up the Environment

Create a GCP Account and set up billing

Install Google Cloud SDK

Authenticate with GCP using

gcloud auth loginCreate a new project using GCP Console or

gcloudCLI

Step 2: Developing the Application

Set up a local development environment with Node.js and Postgres

Develop the application locally on an IDE like VSCode

Test the application thoroughly

Step 3: Preparing for Deployment

Create a Dockerfile for containerization

Set up Cloud Build for CI/CD

Configure Cloud Run or Kubernetes Engine for hosting

Set up Cloud SQL or use a third-party service

Step 4: Deployment

Push code to a Git repository

Trigger Cloud Build to create a container image

Deploy the container to Cloud Run or Kubernetes Engine

Configure networking and security settings

Set up custom domain (if needed)

Step 5: Monitoring and Maintenance

Set up Cloud Monitoring

Configure logging with Cloud Logging

Set up alerts for potential issues

Challenges

Prototyping and going from 0-1 takes too long

Steep learning curve for GCP services

Complex configuration process

Potential for unexpected costs

Requires understanding of containerization and cloud architecture

Security is an after thought

The New Way: Replit

Step 1: Setting Up the Environment

Create a Replit account (can use GitHub or Google for quick signup)

Choose "Node.js" as the template for a new repl

Step 2: Developing the Application

Write code directly in the Replit IDE while pairing with your team

Use the built-in package manager to add Express.js and serverless Postgres

Develop and test the application in real-time

AI chat and code fix are built in no external signups necessary

Step 3: Database Setup

Use Replit's built-in Postgres database (available with just a few clicks)

Configure the connection string in the application

Step 4: Deployment

Click the "Run" button to deploy test the application

Replits built in deployment function to deploy to standard .replit domain or a custom domain

Replit automatically provides a public URL for the application

Step 5: Monitoring and Maintenance

Use Replit's built-in console for logs

Leverage Replit's always-on functionality to keep the app running

Advantages

No need for local setup or installation

Integrated development and deployment environment

Built-in database solution

Instant deployment with a few clicks

Collaboration features for team development

Free tier available for learning and small projects

Security is built in and managed beyond shared responsibility

The Impact

This disruption in cloud services is having far-reaching effects:

1. Accelerated Innovation: Easier access to cloud resources is enabling faster development and deployment of new ideas.

2. Empowering Small Teams: Startups and individual developers can now leverage powerful cloud infrastructure without significant upfront investment.

3. Education and Skill Development: Simplified platforms are making it easier for newcomers to learn cloud computing concepts.

4. New Business Models: The accessibility of cloud services is enabling new types of businesses and applications.

Just as fintech companies abstracted away the complexities of financial services, these new cloud platforms are simplifying access to on-demand compute resources. They're enabling the next generation of creators to build and scale applications more easily than ever before, potentially leading to a new wave of innovation in the tech industry.

The rise of AI empowers these companies to not only simplify cloud services but also to create intelligent platforms that actively assist developers throughout the entire development lifecycle. This AI-powered approach further democratizes access to advanced cloud capabilities, enabling a broader range of creators to build sophisticated, scalable applications with ease. As AI continues to evolve, we can expect these platforms to become even more intuitive, efficient, and powerful, potentially reshaping the landscape of cloud services across the SDLC.

Conclusion

Cloud computing is hitting its "fintech moment" ripe for disruption and innovation. Unlike the limited opportunities in traditional banking, the cloud's potential is vast and ever-expanding. For aspiring founders, this is the golden era to innovate and add real value. The PaaS space isn't mature yet—there's ample room for groundbreaking companies to redefine the future. Come let’s turn Cloud into Banks!